Corporate Partnership May Avoid the Paragraph 125(5.1)(b) Grind

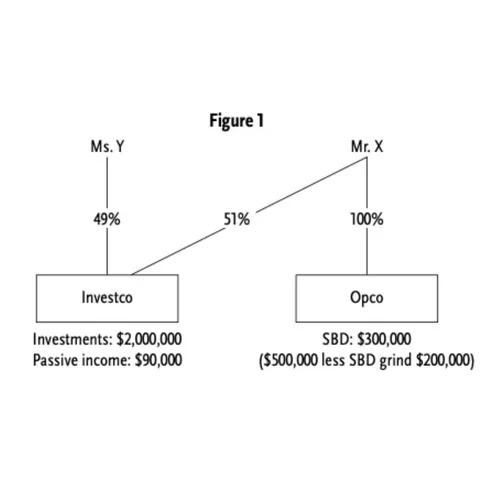

The 2018 federal budget added paragraph (b) to subsection 125(5.1) to penalize certain CCPCs that earn excessive invest- ment income.

The 2018 federal budget added paragraph (b) to subsection 125(5.1) to penalize certain CCPCs that earn excessive invest- ment income.